The United States Supreme Court declared the tariffs imposed by Donald Trump unlawful and revoked them. However, this decision cannot be regarded as the end of the United States’ aggressive trade policies. The President still retains the ability to reimpose tariffs through alternative legal avenues.

Author: Sajjad Sheikhi

The United States Supreme Court declared the tariffs imposed by Donald Trump unlawful and revoked them. However, this decision cannot be regarded as the end of the United States’ aggressive trade policies. The President still retains the ability to reimpose tariffs through alternative legal avenues.

This issue is significant because, concurrent with sweeping tax cuts under the legislation known as the One Big Beautiful Bill, the removal of tariff revenues could expose the government to a substantial budget deficit. Therefore, the return of tariffs albeit under a different structure remains a plausible scenario.

Uncertainty regarding what the replacement tariffs will entail and how the mechanism for reimbursing previously collected duties will be implemented has introduced a new wave of uncertainty into the financial markets.

Why Did Donald Trump Impose Tariffs?

A tariff is a tax on imports that is implemented within the framework of protectionist policies with the objective of strengthening domestic production. In theory, this instrument can contribute to improving the quality of domestic output and increasing employment; however, in practice, higher input costs and pressure on producers’ profit margins are among its consequences. As a result, the impact of tariffs on inflation and unemployment requires careful structural assessment.

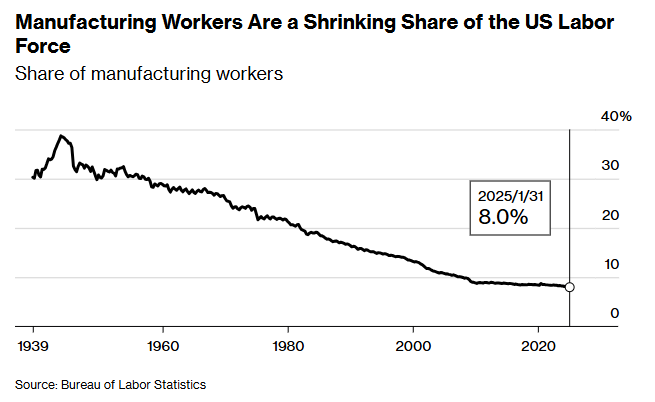

Trump’s primary objective was to revive the U.S. industrial sector. The share of manufacturing in the United States’ gross domestic product has declined in recent decades to approximately 8 percent, whereas this share exceeded 30 percent in the 1950s. This policy was defined within the framework of the administration’s 3 percent economic growth agenda, a program that requires the simultaneous strengthening of both the services and industrial sectors.

However, in 2025, the tariffs triggered significant volatility in the financial markets and, by increasing goods inflation, slowed the pace of interest rate cuts by the Federal Reserve.

Legal Basis for the Revocation of the Tariffs

The tariffs had been imposed under the International Emergency Economic Powers Act (IEEPA) of 1977. The Supreme Court argued that this statute does not grant the President the authority to impose trade tariffs and that, under the Constitution, the power to levy taxes and duties rests with Congress.

As a result:

The imposed tariffs were declared unlawful.

The issue of refunding approximately $170 billion in collected duties was raised.

The mechanism and timeline for reimbursement have become a new source of uncertainty.

Alternative Legal Instruments for Reimposing Tariffs

Despite the Supreme Court’s ruling, other statutes provide avenues for imposing tariffs:

1. Section 122 of the Trade Act of 1974

Authorizes the imposition of tariffs of up to 15% for a period of 150 days in the event of a serious balance of payments deficit.

2. Section 232 of the Trade Expansion Act of 1962

Permits tariffs on national security grounds; requires an investigation by the Department of Commerce (with a 270 day deadline).

3. Section 201 of the Trade Act of 1974

Applicable in cases of serious injury to domestic industries; requires an investigation by the International Trade Commission (ITC).

The initial duration is four years (extendable up to eight years).

4. Section 301 of the Trade Act of 1974

In response to discriminatory trade practices of other countries; without a specified cap.

5. Section 338 of the Tariff Act of 1903

Countering unfair trade practices; with a 50% cap.

In response to the court ruling, Trump, citing Section 122, imposed a 10% global tariff and subsequently increased it to 15%. These tariffs are temporary and subject to a 150 day time limit.

Economic and Financial Implications

i mage

1. Budget Deficit and the Bond Market

If tariff revenues are not fully replaced, the government will be compelled to issue debt. This development:

Increases Treasury yields.

Intensifies pressure on the repo market.

May lead to higher market interest rates without direct action by the central bank.

2. Impact on Inflation and Monetary Policy

The reimbursement of tariffs and the potential increase in the budget deficit may create upward pressure on inflation. Under such circumstances, a rate hold approach by the Federal Reserve would be more likely; similar to the policy at the beginning of 2025, when rates were kept unchanged until trade policy became clearer.

3. Impact on Household Income

In a scenario of complete tariff removal, estimates (including Bloomberg estimates) indicate that real household income could increase by approximately $1,200. This increase, together with reimbursements, could serve as a driver of consumer demand in 2026.

4. Financial Market Implications

Continued uncertainty:

Pressure on the U.S. dollar, Treasuries, and U.S. equities

Strengthening of non U.S. markets and emerging economies

Increased attractiveness of safe haven assets such as gold, the Swiss franc, and the Japanese yen

Conclusion

The repeal of Trump’s tariffs constitutes a significant legal development, but it does not mark the end of the trade war. To prevent a substantial budget deficit, the U.S. government will be compelled to utilize alternative instruments.

In the short term, this situation preserves an environment of uncertainty in the global economy and may lead to increased volatility in financial markets. The future trajectory of markets will depend on the clarity of trade policies, the method of replacing tariff revenues, and the response of the monetary policymaker.