The U.S. employment report once again caught markets off guard. While recent weeks had shown signs of a gradual slowdown in the labor market across supplementary data, and many economists had warned of a deceleration in hiring momentum, the NFP report exceeded expectations in nearly all components. This data not only calls into question the scenario of a rapid interest rate cut, but also challenges the arguments of officials inclined toward expansionary policy and even the future policy path of the Federal Reserve

Author: Sajjad Sheikhi

The U.S. employment report once again caught markets off guard. While recent weeks had shown signs of a gradual slowdown in the labor market across supplementary data, and many economists had warned of a deceleration in hiring momentum, the NFP report exceeded expectations in nearly all components.

This data not only calls into question the scenario of a rapid interest rate cut, but also challenges the arguments of officials inclined toward expansionary policy and even the future policy path of the Federal Reserve.

Dissecting the Report; Strength in Both the Headline and the Details

The strength of the report was not limited to its headline figure; the underlying details also presented a relatively solid picture of the labor market.

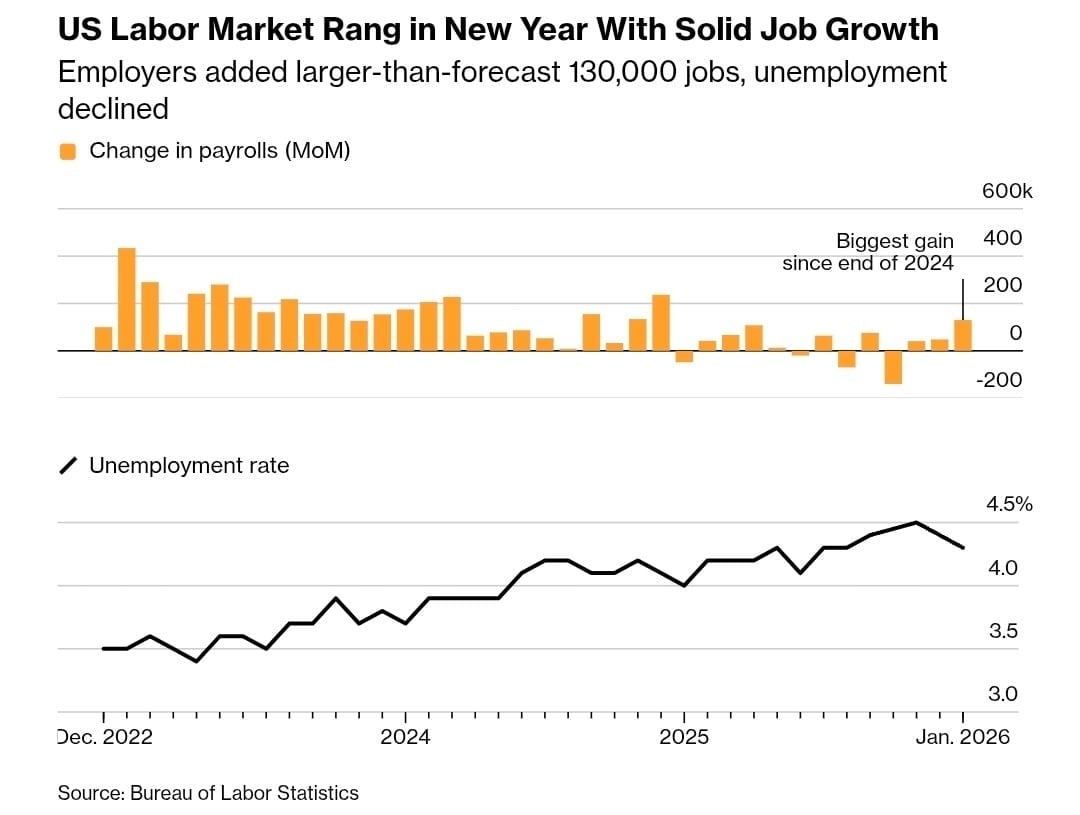

New Employment:In January, 130,000 jobs were created—a figure significantly above the forecast of 69,000.

Unemployment Rate:It declined from 4.4% to 4.3%.

Hourly Wages:Growth came in above expectations, which, alongside tax refunds, could support consumer spending in the first quarter.

The decline in the unemployment rate alongside rising wages is consistent with labor economics theory, as a reduction in labor supply increases its value. These developments come after a significant downward revision of the 2025 data and suggest that the labor market is attempting to stabilize at the beginning of 2026.

Moreover, greater clarity regarding the Trump administration’s tariff policies, along with the implementation of three previous rate cuts, has likely encouraged some employers to resume hiring a development that aligns with Powell’s remarks at the January meeting regarding the “stabilization of the labor market.”

Complementary Signals from the Labor Market

1. Increase in the Participation Rate

The participation rate rose to 62.5%. A simultaneous increase in participation and decline in unemployment is a positive sign; it indicates that job seekers have been absorbed into the labor market. However, delays in the release of population data due to the government shutdown have introduced some uncertainty regarding the accuracy of this component.

2. Decline in Broad Unemployment (U6)

The U6 measure fell from 8.4% to 8%. This index provides a more comprehensive picture, as it includes discouraged workers and those involuntarily employed part time. The decline in this measure confirms a qualitative improvement in the labor market.

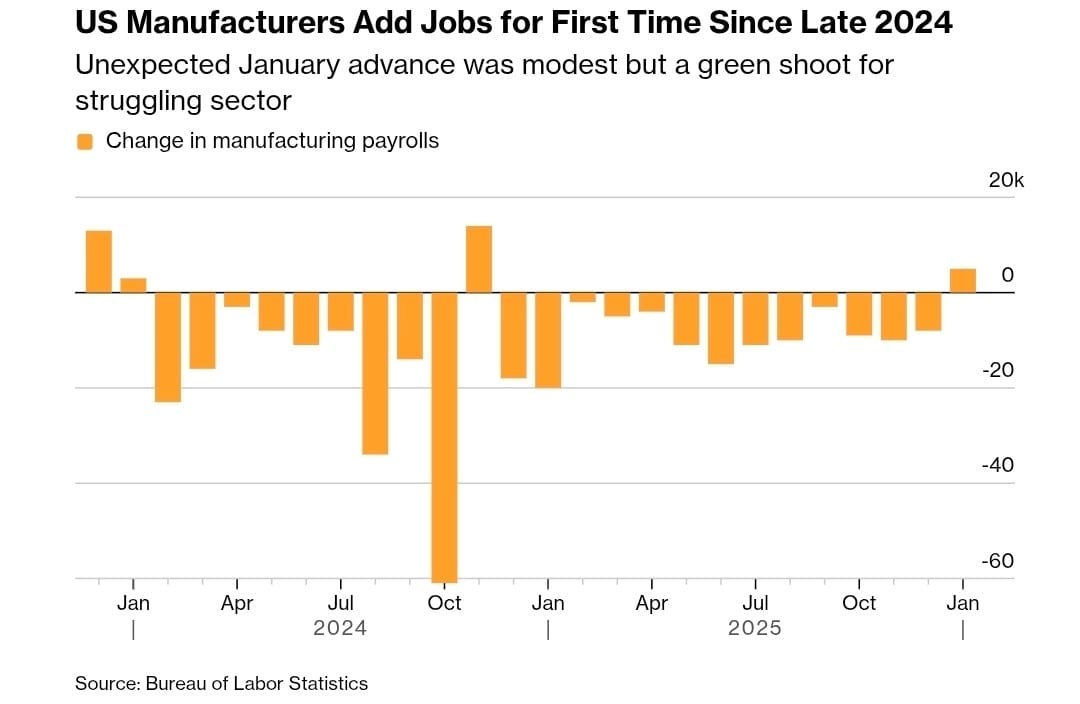

3. Recovery of the Industrial Sector

After a prolonged period of contraction, the industrial sector once again experienced employment growth. Although this growth has been limited, it holds significant importance from a business cycle perspective and may influence estimates of economic growth.

4. Increase in Voluntary Job Quits

An increase in the number of individuals who have voluntarily left their jobs is a sign of confidence in finding new opportunities; this indicator is typically correlated with a healthy labor market.

5. Decline in Involuntary Part Time Employment

A reduction in part time work for economic reasons, alongside a renewed decline in government employment, indicates relative stability in household income conditions.

The Shadow of 2025 Revisions Over the Overall Picture

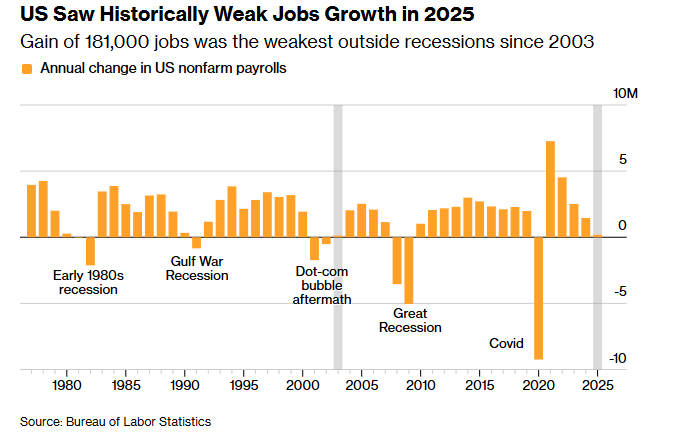

Despite the strong start to 2026, the broad downward revision of the 2025 data presents a different picture. In the entirety of 2025, only 180,000 jobs were created the weakest performance since 2003.

The uncertainty stemming from tariffs and elevated interest rates played a central role in this performance. Companies largely absorbed the impact of tariffs through their profit margins, with the consequences becoming more evident in the labor market than in inflation indicators.

Another important point is the high concentration of employment in the healthcare sector. In January, 124,000 of the total jobs created were attributable to this sector. Although this industry is noncyclical in nature and continues hiring even during downturns, excessive reliance on it cannot serve as an accurate measure of the overall health of the economy; moreover, productivity in this sector is generally assessed as relatively lower.

Monetary Policy Implications; Will Rate Cuts Be Delayed?

The unexpected improvement in the labor market limits the Federal Reserve’s room to maneuver in cutting interest rates. Although it is not reasonable to rely on a single data point, the consistency of the report’s details reduces the likelihood that it is merely statistical noise.

Following the release of the report, traders lowered the probability of a rate cut at the June meeting to below 50%. Powell had previously cited the stabilization of the labor market as a reason to maintain current rates, and this argument has now been reinforced.

Even if inflation continues to decline gradually, a strong labor market could reignite price pressures, prompting the Federal Reserve to exercise greater caution in adopting an expansionary policy stance.

Impact on the Dollar, Euro, and Gold

If strong employment data persist, the likelihood of a rate cut diminishes, and the Federal Reserve’s restrictive stance combined with the United States’ superior economic growth relative to other G7 members would support a stronger dollar.

In the short term, the dollar is positioned to outperform, while the euro may remain under pressure. However, gold, driven by independent fundamental catalysts such as central bank demand (particularly from China) and geopolitical risks, retains the capacity to sustain a gradual upward trend.

Federal Reserve Independence in the Face of Political Pressure

Trump’s remarks regarding the need to maintain the lowest interest rates in the world lack operational grounding from a monetary policy perspective. The Federal Reserve’s mandate is not to finance the government, but to manage inflation and ensure employment stability. Decisions regarding interest rates whether made by Kevin Warsh or any other chair are based on economic data, not political pressure.

Conclusion

The January employment report presented a stronger than expected picture of the U.S. labor market and revealed signs of stabilization. This data reduces the likelihood of an early rate cut and has reinforced the Federal Reserve’s cautious stance.

As a result, market expectations for expansionary policy have been adjusted, and the dollar stands to benefit in the near term.